When interest rates are high, people are supposed to consider twice to borrow. When you are low, they are supposed to come out with a metaphoric credit card (or craftsmanship). This is it Central idea Supports the monetary policy of central banks.

Of course, central banks determine the interest rate in the short term only. Bond proceedsWhile it is based on the prices of the central bank, it is established in the secondary market through a kind of continuous auction process. In a world in which the revenues of government bonds describe the potential path to take the procedures of the future central bank, the government must be indifferent to the place where this curve is issued.

This, according to two recent long reports by strategies, rates, Main Islam in Barclays and Mark Capliton from Bank of America – is not the world in which we live.

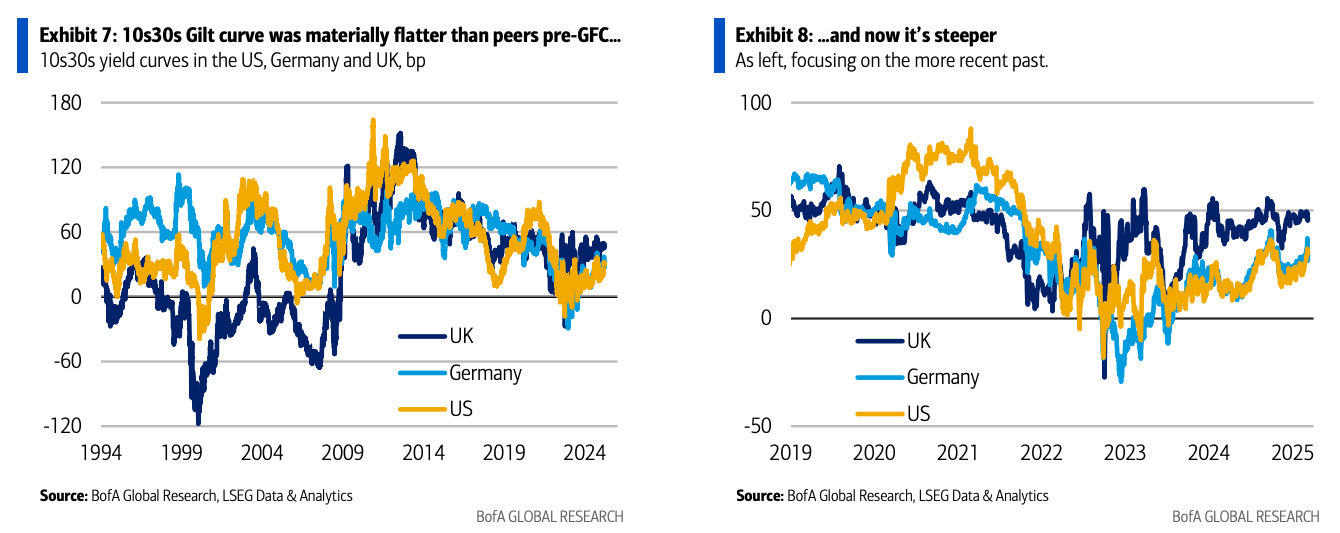

Before the global financial crisis, Gilts often resulted in ten years more than thirty years (contradicts the traditional logic that is longer than the time = more risks = more return). Most types of bonds understood this as a reflection of the constant demand from life insurance companies in the United Kingdom and pension funds that follow investment strategies that depend on responsibility. As such, it makes sense for HM Treasury to convert the debt version for a longer period, meet this request and reduce the so -called “risk of re -financing”. By doing this, the United Kingdom ended with the highest average government bond market.

Quickly forward to the post -judgment era, long -term Gilts trading with return not only 10 years old, but also with a return that spreads over the 10s larger than those in the United States or Germany. Bofa charts:

((High -precision))

{kind=link}

Although “doubts about whether smart sports chromatography can really take bond returns and dismantle it in different component parts that cannot be observed (and perhaps hypothetical), he believes that this new gap represents a great term on a large term-and is known as the long expensive gravity for the government. He copied his look with a set of frontal differences Gilts-Sonia and front-to-spread plans that are an eccentric genius even for FT alphaville.

In Islam, Barclays has no such views about saying directly that the increasing period of Premia “explains the largest part of the step higher in revenue (thirty years).”

Why may this be? A lot depends on Gorilla 800 lbers of the market for the market for Gilts for a long time: whether the long demand for them from the UK pension funds has ended significantly. while ‘The peak LDI“He has It was called Before, the arguments deserve to be spent.

First, the huge shift called “disposal” from stocks to bonds that have been for several shares in the United Kingdom over the past two decades. So it cannot happen again. Capleton, Capleton, the amount of possible disposal of the projection is, according This is the minimum.

Second, with almost all selected pension plans, all of which are closed in front of the new arrivals, people retire and die in the end. This now appears in reducing membership data. As Caspnene writes:

The edition of the “ONS professional plans in the United Kingdom” shows that the total membership decreased by 16 % between the third quarter of 2019 and 1Q 2024, and in the total total, the training progresses, as the percentage of retirees increased from 42 % to 49 % over the same short period.

Third, the current value of the obligations of pension funds was Hole By … height of bond returns. Therefore, if every specific scheme for the benefits is completely invested from its assets in Gilts, this will only represent about a trillion pounds of the request, with a decrease from the ceiling of the demand for about a trillion pounds a few years ago.

The bottom line is that there is no new demand for retirement boxes on Gilts for a long time around the corner. This fact appears in bond prices.

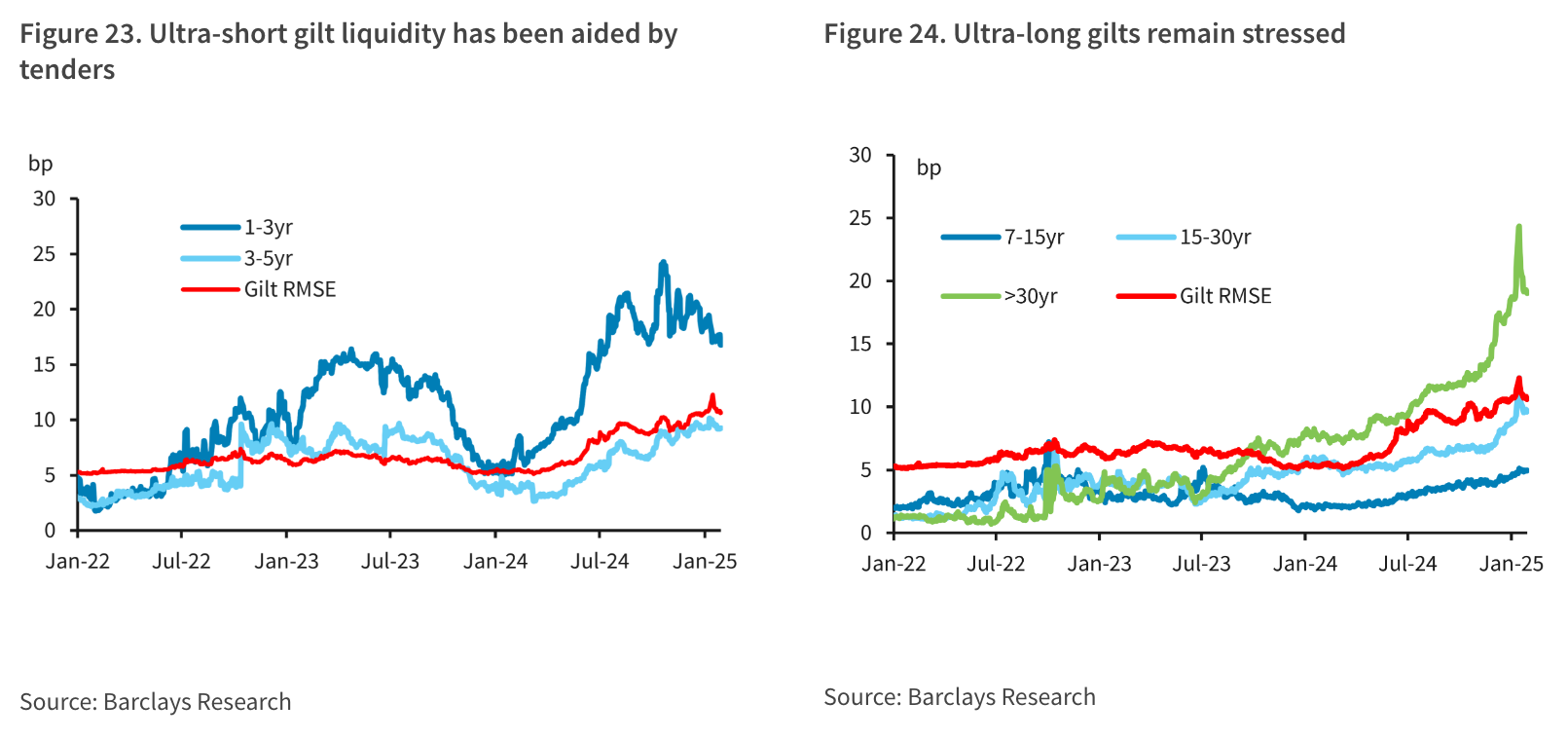

Barclays makes this point with mathematics. While the auctions of the doctrine have gone well, the market’s ability to digest the risks is, as it argues Islam, a function of basic liquidity. One of the ways that Barclays takes a large amount of that is to draw lines along different parts of the doctrine and calculation curve Root average square errors Which is created from these lines is one of the best suitability. The basic intuition is that in a large -scale liquid market, all cells will be judged.

But this does not happen. The curve is part, as this scale of liquidity was deteriorating quickly. last year We indicate To increase the reversal of the curve, it may have to do with the display of the tax -related continuity processes associated with the low -section Gilts. But it seems that something else also happens. Barclays:

((High -precision))

{kind=link}

account:

The issuance of a sect needs to adapt radically and rapidly. … this argues by decreasing materials in the issuance of a long -term sect.

This puts them mainly on the same page as Barclays.

It is not as if governments have not made significant changes before against the background of the bonds that have long been rooted. The older readers will remember that on Halloween in 2001, the US Treasury caused a large link to a large link when that is I cancel all the long version Even another notice. Defending the decision, Peter Fischer, the treasury loaded at the time that:

This relates to the attempt to manage taxpayers wisely. … This is a relatively expensive borrowing tool that is not simply necessary for the current financing requirements or those we expect.

Moreover-CAPLETON mention those under the retirement age in the state-the American move was resonated with Jeffrey Hao’s decision to cancel a long cheerful version in his budget in 1983. Although Barclays strikes the tone The tall wholesale is the one that Bofa believes that DMO should look closely a day.

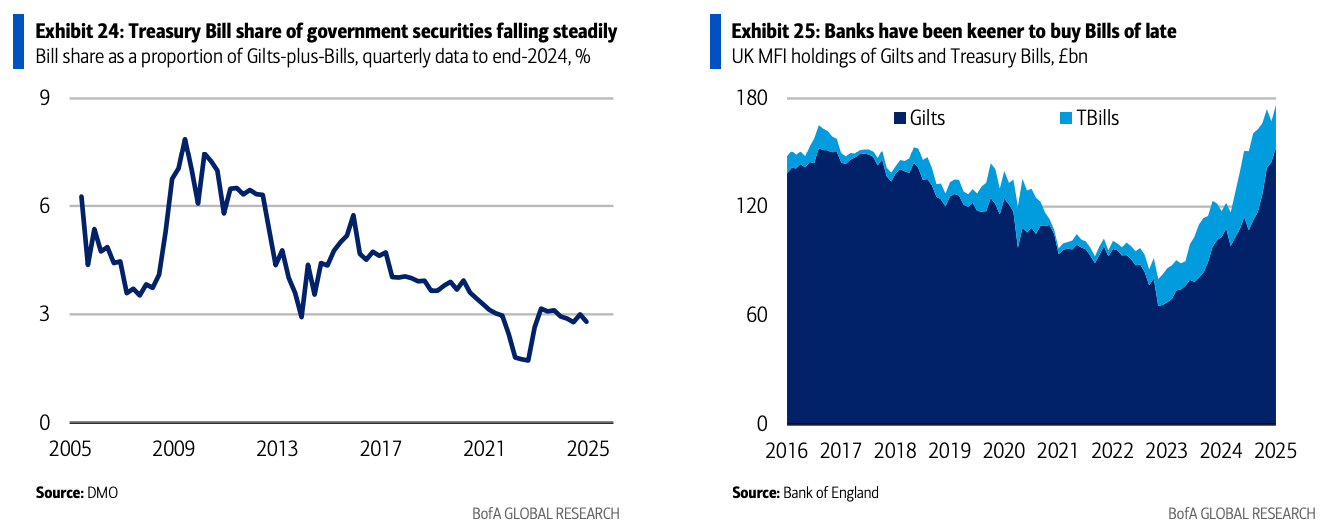

Instead of issuing expensive bonds that have long ago that the main beneficiaries are dying, BOFA defenders turn the release into treasury bills in the UK. The UK’s T-Bill market is great by international standard, and makes Capleton that with the development of quantitative tightening, there will be a great demand for bills from banks looking to find alternative assets that act like Bank of England.

((High -precision))

{kind=link}

Barclays and Bofa alike (Ed: Try to say that several times quickly) Do a good case that the UK government, if it is a company, will re -examine and shorten, the copy of its debt.

Capleton also raises the idea that they should buy Gilts long ago that have been traded with a deep discount, “take profits” on the bonds that are sold on the market with low coupons, and may expel up to 16 percent of the gross domestic debt/product in this process.

But the shark jumps when he writes:

With some of these issues, the clear temptation will be the market consultation. Our main concern about this is the risk of delayed procedure, and perhaps for a long time, if it is a very official advice … we suggest experimental operations rather than full consultations.

Experience instead of consulting? Sorry, we are British.

In general, these two wonderful and fantasy are full of interesting debt management ideas. But whether the UK government responds to the bond market pricing signals in the way in which natural economic agents are supposed to do another question.

Slip: The author has direct possessions between his personal investments, one of which was long ago. 😢

https://www.ft.com/__origami/service/image/v2/images/raw/https%3A%2F%2Fd1e00ek4ebabms.cloudfront.net%2Fproduction%2Fa714a9a1-1b20-49f8-b38c-28511abc82f0.png?source=next-article&fit=scale-down&quality=highest&width=700&dpr=1

Source link